Market-linked growth. Zero risk of loss. Guaranteed income for life. Here is everything South Carolina retirees need to know about the FIA.

If you have ever wished you could earn returns tied to the stock market without actually risking your retirement savings in the stock market — a fixed indexed annuity may be exactly what you have been looking for.

For thousands of South Carolina retirees, the fixed indexed annuity — commonly called an FIA — has become one of the most important retirement tools available today. It sits in a unique category: safer than the stock market, more growth potential than a CD, and capable of generating income you can never outlive.

In this guide, William A. Garland Jr. of PAG Advisory Group in Columbia, South Carolina breaks down exactly what a fixed indexed annuity is, how it works, who it is right for, and what questions to ask before getting one.

What Exactly Is a Fixed Indexed Annuity?

A fixed indexed annuity is an insurance contract between you and an insurance company. You deposit a sum of money — either all at once or over time — and in return, the insurance company promises two things:

- Your principal is completely protected from market losses. No matter what the stock market does, you cannot lose the money you deposited.

- You can earn interest linked to a market index — such as the S&P 500 — when that index performs positively.

Think of it this way: you get to participate in market gains up to a limit, while being completely shielded from market losses. In years when the market index rises, your account earns interest. In years when the market falls, your account simply earns zero — never a negative return.

A fixed indexed annuity is not a stock market investment. Your money is held by an insurance company, not invested directly in the market. The index only determines how much interest gets credited to your account — your principal never fluctuates with the market.

This is what sets FIAs apart from every other market-linked product: the downside is eliminated entirely, while a meaningful upside still exists.

How Does a Fixed Indexed Annuity Work?

Understanding how an FIA actually credits interest is the key to understanding whether it is right for you. Here is the straightforward version:

You Deposit Money

You fund the annuity with a lump sum — from personal savings, a CD rollover, a 401(k) transfer, or an IRA rollover. Some FIAs also accept ongoing contributions over time.

An Index Strategy Is Chosen

You (with guidance from your advisor) choose how your interest will be calculated — typically linked to an index like the S&P 500, a blended index, or a combination of strategies. Most FIAs allow you to divide your money across multiple index strategies.

Interest Is Credited Annually

At the end of each contract year, the insurance company looks at how your chosen index performed. If it rose, your account is credited with interest — up to your product’s cap rate or participation rate. If it fell, you receive 0% for that year. Your principal stays intact either way.

Gains Are Locked In Forever

Here is one of the most powerful features of an FIA: once interest is credited to your account, it is locked in permanently. A future market crash cannot take those gains away from you. You essentially reset at a new, higher floor each year.

Lifetime Income Can Be Activated

When you are ready to retire — or right now if you prefer — you can activate a lifetime income rider (if included in your FIA) to begin receiving a guaranteed monthly paycheck that continues for as long as you live.

The market goes up, you earn interest. The market goes down, you earn nothing — but you lose nothing either. Your gains from prior years are locked in forever.

William A. Garland Jr., PAG Advisory Group — Columbia, SCUnderstanding Cap Rates and Participation Rates

There are two main ways an FIA can limit — or measure — your upside participation in an index. You will want to understand both before choosing a product.

Cap Rate

A cap rate is the maximum percentage of index growth your account can earn in a given year. For example, if your FIA has a 10% annual cap and the S&P 500 rises 18% in a year, your account is credited 10% — not 18%. If the index rises 7%, you earn 7% (under the cap, so you keep it all). If the index falls 15%, you earn 0%.

Participation Rate

A participation rate tells you what percentage of an index’s gain gets credited to your account. If your FIA has a 60% participation rate and the index rises 20%, your account earns 12% (60% of 20%). Some FIAs use participation rates instead of — or in addition to — cap rates.

Spread / Margin

Some FIA strategies use a spread — an amount subtracted from the index gain before crediting. If the index gains 12% and the spread is 2%, you earn 10%. Spreads are less common than caps but worth understanding when comparing products.

Cap rates, participation rates, and spreads directly affect how much you earn in positive market years. An independent advisor like William Garland compares these numbers across multiple carriers to find the product that gives you the best combination of upside potential, protection, and income options.

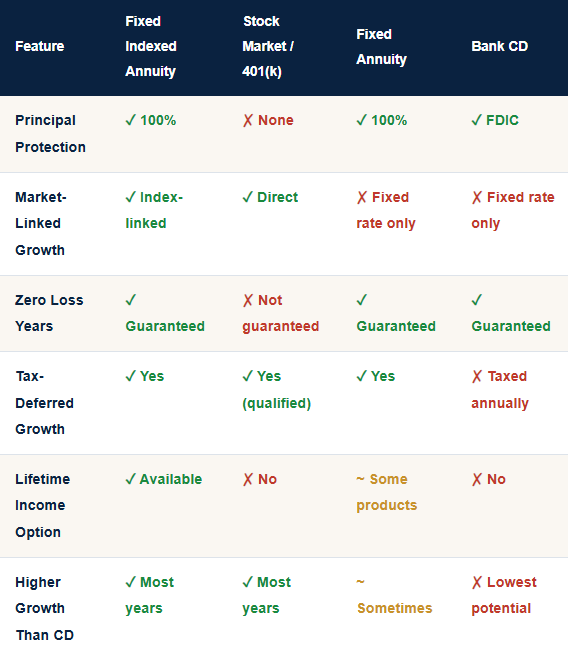

FIA vs. Other Retirement Products

How does a fixed indexed annuity compare to other products you may already have or be considering?

The FIA occupies a unique position in this table: it is the only product that combines principal protection, market-linked growth potential, tax-deferred accumulation, and optional lifetime income — all in one contract.

The Lifetime Income Rider — Your Personal Pension

One of the most powerful features of many fixed indexed annuities is the optional lifetime income rider. For a small annual fee deducted from your account, a lifetime income rider gives you the ability to turn your FIA into a guaranteed paycheck — for as long as you live.

Here is how it typically works:

- Your rider has a separate income benefit base that grows at a guaranteed rate (often 5–7% per year) during your accumulation years — even if your account value grows more slowly due to market caps.

- When you are ready to begin income, you activate the rider and begin receiving a guaranteed monthly payment calculated as a percentage of your income benefit base.

- Those payments continue for as long as you live — even if your account value runs to zero. This is the insurance company’s promise.

- Most riders also include joint-life options, so income continues for your spouse after you pass.

For South Carolina retirees who do not have a traditional employer pension, this feature is transformative. It converts a lump sum of savings into the kind of predictable, reliable monthly income that previous generations took for granted from their employers.

Who Is a Fixed Indexed Annuity Right For?

A fixed indexed annuity is not right for everyone — and an honest advisor will tell you so. Here is a straightforward profile of who benefits most:

FIAs tend to work well for people who:

- Are within 10 years of retirement or already retired

- Cannot afford a significant market loss to their savings

- Want more growth potential than a CD or savings account offers

- Have no employer pension and need to create their own guaranteed income

- Want tax-deferred growth outside a traditional IRA or 401(k)

- Are rolling over a 401(k) and want to protect those funds from future market crashes

- Value financial security and predictability over chasing maximum returns

FIAs may not be the right fit for people who:

- Need access to their full account value within the first few years (most FIAs have a surrender charge period)

- Are early in their careers and can afford to ride out market cycles in growth investments

- Want maximum market returns without any growth limitations

PAG Advisory Group is based in Columbia, South Carolina and serves clients throughout South Carolina. William Garland always starts with a thorough review of your full financial picture before recommending any product — and if an FIA is not right for your situation, he will tell you.

Fixed Indexed Annuities for South Carolina Retirees

South Carolina presents a particularly favorable environment for FIA owners:

- South Carolina does not tax Social Security benefits — and annuity income can be structured to work alongside your Social Security in a tax-efficient way.

- South Carolina has a state guaranty association that provides an additional layer of protection for annuity policyholders beyond the insurance company’s own claims-paying ability.

- The cost of living in Columbia, Greenville, Charleston, and across South Carolina makes a well-structured guaranteed income plan highly achievable — you do not need an enormous account to fund a comfortable retirement here.

William A. Garland Jr. has spent 27+ years working exclusively with South Carolina retirees, and he designs every FIA strategy with the specific financial landscape of this state in mind.

Key Terms Every FIA Buyer Should Know

Fixed Indexed Annuity Glossary

Cap Rate

The maximum annual interest rate your account can earn, regardless of how much the index gains.

Fixed Indexed Annuity Glossary

Cap Rate

The maximum annual interest rate your account can earn, regardless of how much the index gains.

Participation Rate

The percentage of an index’s gain that is credited to your account. A 70% participation rate means if the index gains 10%, you earn 7%.

Floor

The minimum interest rate you can earn in any year — for most FIAs, this is 0%. Your account can never go negative due to market losses.

Surrender Charge Period

A period (usually 5–10 years) during which withdrawing more than a specified free amount triggers a charge. After this period, your money is fully accessible.

Lifetime Income Rider

An optional feature (usually at an additional cost) that guarantees a monthly income payment for as long as you live, regardless of account value.

Income Benefit Base

A separate, often higher value used to calculate your lifetime income payments — typically grows at a guaranteed rate during the accumulation phase.

Free Withdrawal

The percentage of your account value (usually 10% per year) you can withdraw penalty-free even during the surrender charge period.

Annuitization

Converting your annuity into a stream of regular payments. With a lifetime income rider, this is not always required — you receive income without giving up ownership of the account.

Questions to Ask Before Buying an FIA

Not all fixed indexed annuities are the same. Before signing anything, make sure you get clear answers to these questions from your advisor:

- What is the current cap rate, and can the insurance company change it after I purchase?

- What is the surrender charge schedule, and how long is the surrender period?

- How much can I withdraw each year without penalty?

- What is the financial strength rating of the issuing insurance company?

- Is there a lifetime income rider available, and what does it cost annually?

- What happens to my account balance when I die — can it pass to my beneficiaries?

- How is interest credited — annually, monthly, or at another interval?

- Am I buying this from an independent advisor who can compare multiple carriers, or from a captive agent who can only offer one company’s products?

William Garland at PAG Advisory Group is an independent advisor — meaning he is not tied to any single carrier. He compares FIA products across dozens of top-rated insurance companies to find the one that offers the best cap rates, income options, and financial strength for your specific situation.

Next Steps: Talk to a South Carolina FIA Specialist

A fixed indexed annuity is not a simple off-the-shelf purchase — the right product depends on your age, income needs, existing savings, tax situation, and retirement timeline. Getting independent advice from someone who has compared hundreds of FIA products across dozens of carriers is essential.

PAG Advisory Group is based in Columbia, South Carolina and serves clients throughout South Carolina — including Greenville, Charleston, Spartanburg, Sumter, Rock Hill, Florence, Lexington, and Fort Jackson military families. William A. Garland Jr. offers a free, no-obligation retirement income review that includes a personalized FIA analysis for your specific situation.

There is no pressure and no cost. Just a clear, honest conversation about whether a fixed indexed annuity belongs in your retirement plan — and if so, which one gives you the best outcome.